When a depreciable asset is sold the sales price is?

When you sell a depreciated asset, any profit relative to the item’s depreciated price is a capital gain. For example, if you buy a computer workstation for $2,000, depreciate it down to $800 and sell it for $1,200, you will have a $400 gain that is subject to tax.

How does depreciation affect the basis of an asset?

Whenever you claim depreciation, it reduces the tax basis of the asset in question. When you sell the asset, your gain will be equal to the sales proceeds minus the asset’s tax basis. You therefore have no gain or loss on the sale.

What is depreciable asset?

A depreciable asset is property that provides an economic benefit for more than one reporting period. A qualifying asset is initially classified as an asset, after which its cost is gradually depreciated over time to reduce its book value.

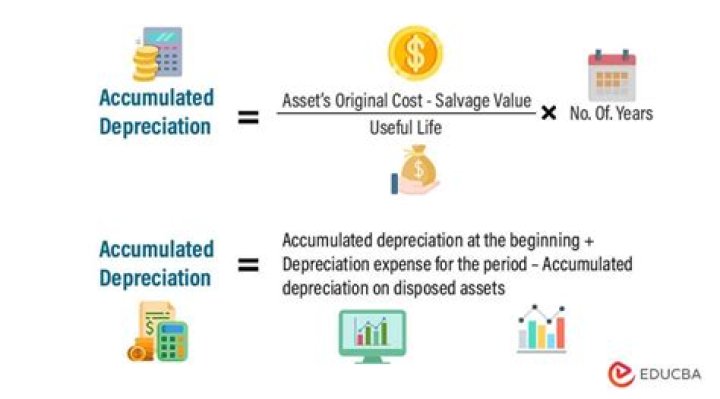

How much can you depreciate an asset?

There are two estimates needed: 1) the number of years that the asset will be used, and 2) the salvage value at the end of the asset’s use. If an asset has a cost of $100,000 and is expected to be used for 10 years and then have no salvage value, most companies will depreciate the asset at the rate of $10,000 per year.

When was no depreciation claimed on an asset?

1. Asset on which no depreciation was ever claimed, could not be assessed u/s 50. v During relevant A.Y., assessee sold certain plant & machinery (not in use) which was partly acquired in year 1997-98 and partly in year 1998-99.

Are there special provisions for capital gains in case of depreciable assets?

“Special provision for computation of capital gains in case of depreciable assets. 50.

Can a sale of land be a depreciable asset?

Applicability of Section 50 in case of Sale of Land Since land is not a depreciable asset & it cannot form part of block of assets in absence of rate of depreciation having been prescribed therefore, provisions of section 50 cannot be invoked in case of sale of land.

Do you have to have same percentage of depreciation for all assets?

Only requirement is that in respect of assets which form block of assets, same percentage of depreciation should be prescribed. All assets, which may be of different types, but in respect of which same percentage of depreciation is prescribed, are to be treated and form part of block of assets.