When should closing entries be made?

Closing entries take place at the end of an accounting cycle as a set of journal entries. The closing entries serve to transfer the balances out of certain temporary accounts and into permanent ones. This resets the balance of the temporary accounts to zero, ready to begin the next accounting period.

Should closing entries be made before or after preparing financial statements?

They must be done before you can prepare your financial statements and income tax return. Closing entries are needed to clear out your revenue and expense accounts as you start the beginning of a new accounting period. Preparing your closing entries is a very simple, mechanical process.

Why do we prepare closing entries at year end?

The purpose of closing entries is to prepare the temporary accounts for the next accounting period. In other words, the income and expense accounts are “restarted”. After preparing the closing entries above, Service Revenue will now be zero. The expense accounts and withdrawal account will now also be zero.

Are closing entries necessary?

The purpose of the closing entry is to reset the temporary account balances to zero on the general ledger, the record-keeping system for a company’s financial data. All revenue and expense accounts must end with a zero balance because they are reported in defined periods and are not carried over into the future.

When closing entries are made all?

Making closing entries means creating a zero balance in all temporary accounts by carrying those balances over to permanent accounts. This prepares the books for the next accounting period to start.

Are closing entries done monthly?

Accountants may perform the closing process monthly or annually. The closing entries are the journal entry form of the Statement of Retained Earnings.

What do closing entries do to an account?

Definition of Closing Entries. Closing entries transfer the balances from the temporary accounts to a permanent or real account at the end of the accounting year. As a result, the temporary accounts will begin the following accounting year with zero balances.

When do you close a journal entry in accounting?

Closing entries, also called closing journal entries, are entries made at the end of an accounting period to zero out all temporary accounts and transfer their balances to permanent accounts. In other words, the temporary accounts are closed or reset at the end of the year. This is commonly referred to as closing the books.

How are retained earnings used in closing entries?

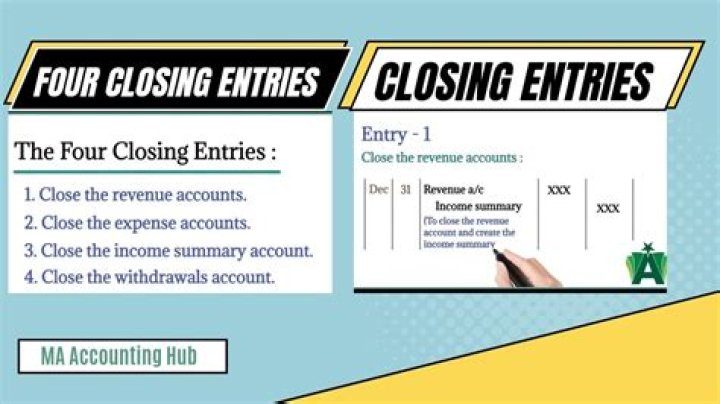

Retained Earnings are part , which is a permanent account on the balance sheet. The income summary is a temporary account used to make closing entries. All temporary accounts must be reset to zero at the end of the accounting period. To do this, their balances are emptied into the income summary account.

How is an income summary used in a closing entry?

A closing entry involves the use of the account income summary. Income summary is a holding account used to aggregate all income accounts except for dividends expense. Income summary is not reported on any financial statements because it is only used during the closing process, and at the end of the closing process, the account balance is $0.