When to use predetermined overhead rate in accounting?

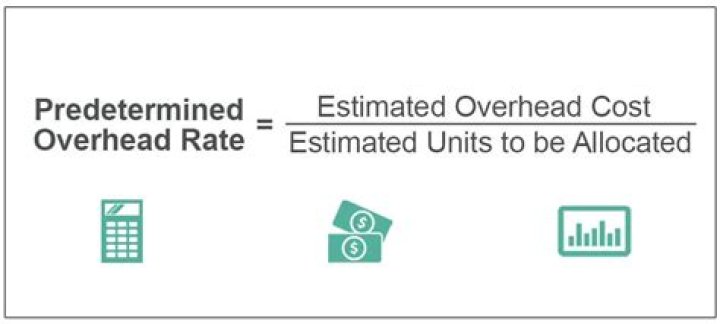

Predetermined overhead rate. Predetermined overhead rate is used to apply manufacturing overhead to products or job orders and is usually computed at the beginning of each period by dividing the estimated manufacturing overhead cost by an allocation base (also known as activity base or activity driver).

How to calculate predetermined overhead rate for direct labour?

Total of direct material or direct labour will give you manufacturing cost. Then, divide the amount of MOH cost to Direct labour. It would give you predetermined overhead rate. Therefore, you would multiply that rate with direct labour since the company uses direct labour cost as allocation base.

How to calculate the overhead rate for the Assembly Dept.?

The actual manufacturing overhead for the year was $123,900 and actual total direct labor was 21,000 hours. compute predetermined overhead rate for the year. if the ques. states that it has more than one departments, eg. an assemble dept and gives m/overhead,DLC, DLL,and machine hours. how do i calculate the overhead rate for the assembly dept.?

When do you eliminate the difference between overhead and applied overhead?

This difference is eliminated at the end of the period. The elimination of difference between applied overhead and actual overhead is known as disposition of over or under applied overhead. The predetermined overhead rate computed above is known as single predetermined overhead rate or plant-wide overhead rate. It is mostly used by small companies.

Is the predetermined overhead rate a realistic assumption?

The mechanism which is used to calculate the predetermined overhead rate is an assumption based therefore many cost accountant and financial analyst claims that it is not realistic and thus should not be the basis for any allocation of overheads.