When would you use a generation-skipping trust?

A generation-skipping trust helps you transfer money and assets to someone who is at least 37.5 years younger than you, while minimizing estate taxes. and how we make money. A generation-skipping trust is used to transfer money or other assets to someone who is at least 37.5 years younger than you.

What makes a trust generation-skipping?

A generation-skipping trust is a type of trust that designates a grandchild, great-niece or great-nephew or any person who is at least 37 ½ years younger than the settlor as the beneficiary of the trust. The goal of a generation-skipping trust is to eliminate one round of estate tax.

Who controls a generation-skipping trust?

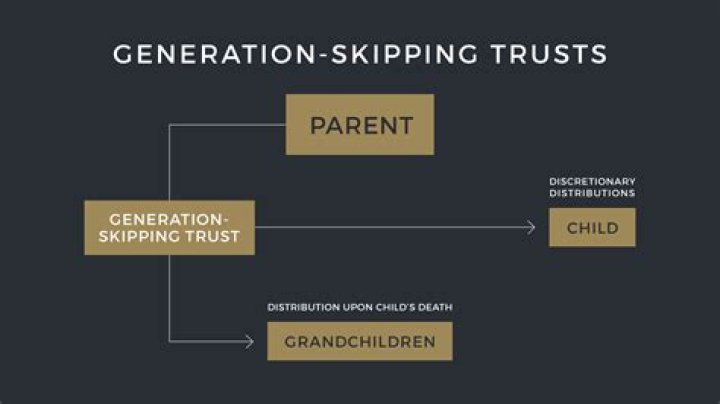

The children retain virtually full control of their trusts during their lifetimes. None of the assets of the Generation-Skipping Trust are includable in the estate of the child on their death and pass free of estate tax and generation-skipping tax to their children or designated beneficiaries.

Can a trust skip a generation?

A generation-skipping trust (GST) is a type of legally binding trust agreement in which the contributed assets are passed down to the grantor’s grandchildren, thus “skipping” the next generation, the grantor’s children.

What is the skip generation?

Definition of Skipped Generation Family (noun) A family in which grandparents raise grandchildren due to the absence of parents.

Are any present or future trust beneficiaries skip persons?

Grandchildren and great-grandchildren are the most common skip persons. But under the deceased parent rule (IRC § 2651(e)), descendants are moved up to their parent’s level if the parent dies before the date of transfer.

What is generation skipping tax exemption?

The Generation-Skipping Tax Exemption An exemption is an amount that can be directly transferred to grandchildren or into a generation-skipping trust for the benefit of grandchildren without incurring a federal GST. Any gifts made over that amount were subject to a 35% tax rate.

How many generations can a trust last?

To oversimplify, the rule stated that a trust couldn’t last more than 21 years after the death of a potential beneficiary who was alive when the trust was created. Some states (California, for example) have adopted a different, simpler version of the rule, which allows a trust to last about 90 years.

When do you need a generation skipping Trust?

Generation-skipping trusts are effective wealth-preservation tools for individuals with significant assets and savings. A generation-skipping trust (GST) is a legally binding agreement in which assets are passed down to the grantor’s grandchildren—or anyone at least 37½ years younger—bypassing the next generation of the grantor’s children.

Can a GST be removed from a generation skipping Trust?

It may sound like GSTs cannot provide any financial advantages to a grantor’s children, but on the contrary, the grantor can give his or her children access to any income the trust’s assets generate without removing the assets from the GST.

Is there a tax exemption on generation skipping?

The American Taxpayer Relief Act of 2012 established a permanent $5 million tax exemption on generation-skipping transfers, meaning there’s only a federal tax on a generation-skipping transfer of wealth exceeding the amount of $5 million. This amount adjusts every year to account for inflation.

Can a grantor of a trust create a GST?

If your family already has a GST and you are the grantor’s child, you may want to create a GST for your own grandchildren. This way, the chain of trusts minimizes the tax liability for your family in generations to come. Kevin O’Flaherty is a graduate of the University of Iowa and Chicago-Kent College of Law.