Where does bad debt go on financial statements?

Bad debt expenses are generally classified as a sales and general administrative expense and are found on the income statement. Recognizing bad debts leads to an offsetting reduction to accounts receivable on the balance sheet—though businesses retain the right to collect funds should the circumstances change.

How do you write-off bad debt in a profit and loss statement?

Sometimes, a debt written off in one year is actually paid in the next year – a debit to cash and a credit to irrecoverable debts recovered. The credit balance on the account is then transferred to the credit of the statement of profit or loss (added to gross profit or included as a negative in the list of expenses).

Where does bad debt expense go on a profit and loss statement?

Bad debt expense, the companion to bad debt reserves, shows on the profit and loss statement. A bad debt reserve is the amount that companies set aside to cover uncollectible receivables, notes or loans.

How are bad debts recorded in an account?

The Pioneer Ltd will record the following entries to give effect to bad debts in its books of accounts: Profit and Loss A/c DR. All expenses which are not directly related to the main business activity will be reflected in the Profit & Loss A/c. These are mainly the administrative, selling and distribution expenses.

How does the provision for bad debts work?

Provision for Bad Debts (P&L) Credit: Provision for Bad Debts. The debit account is charged against current years profit and the credit head is shown as a deduction from. debtors in the balance sheet. PRESENTATION OF PROVISION FOR BAD DEBTS. Extract of P&L to show the Provision.

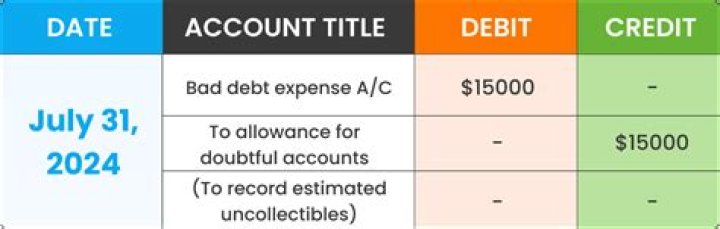

How is bad debt expense recorded in a journal?

Estimate uncollectible receivables. Record the journal entry by debiting bad debt expense and crediting allowance for doubtful accounts. Allowance for Doubtful Accounts The allowance for doubtful accounts is a contra-asset account that is associated with accounts receivable and serves to reflect the true value of accounts receivable.