Which accounting concept applies when a work sheet is prepared at the end of each fiscal cycle to summarize the general ledger information needed to prepare financial statements P 214?

Accounting- Eval. #8

| Question | Answer |

|---|---|

| Closing entry for owner’s drawing account. | Credited. |

| Which accounting concept applies when a worksheet is prepared at the end of each fiscal cycle to summarize the journal Ledger information needed to prepare financial statements? (A) Accounting Period Cycle (B) Consistent Reporting. | B. |

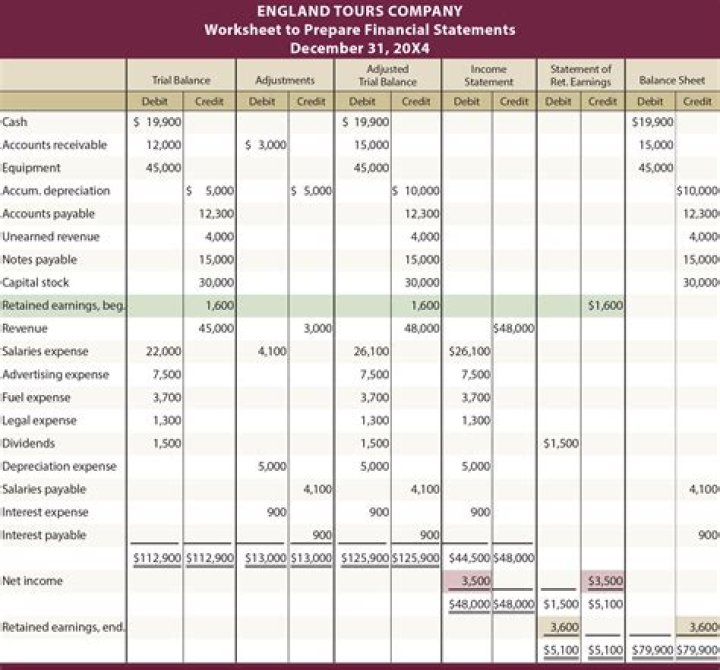

Why is a worksheet prepared at the end of a fiscal period?

The worksheet is not a permanent account. It is not a part of a journal or ledger. It is a device used for easy preparation of adjusting entries and financial statements. The worksheet is prepared at the end of the accounting period before the preparation of financial statements.

What is the balance of each temporary account at the end of each fiscal period?

At the end of a fiscal period, the balances of temporary accounts are summarized and transferred to the owner’s capital account. Temporary accounts must start each fiscal period with a zero balance. Journal entries used to prepare temporary accounts for a new fiscal period are closing entries.

What type of accounts are used to accumulate information from one fiscal period to the next?

Accounts used to accumulate information from one fiscal period to the next are called permanent accounts. Permanent accounts are also referred to as real accounts.

Are worksheets prepared in pen?

Terms in this set (28) A work sheet is prepared at the end of each fiscal period. The work sheet is a working paper and is prepared in pen. After the net loss is calculated, it should be reflected in the debit column of the Income Statement section and the credit column of the Balance Sheet section.

What group of accounts are included in the temporary accounts?

Temporary accounts include revenue, expense, and gain and loss accounts.