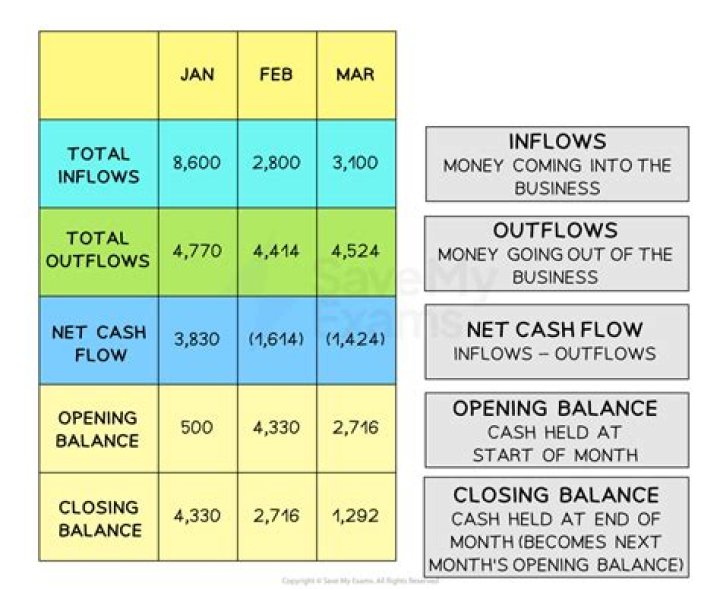

Which accounting method is best for keeping track of cash inflows and cash outflows?

Using the accrual method gives you a good idea of the cash inflows and outflows you can expect for a given period and plan your cash management accordingly. You can see the changes in your cash balances by running a Cash Flow Statement.

How the bank reconciliation can be used as an internal control tool for cash?

Bank reconciliations are an essential internal control tool and are necessary in preventing and detecting fraud. They also help identify accounting and bank errors by providing explanations of the differences between the accounting record’s cash balances and the bank balance position per the bank statement.

Why is it important for a bank account holder to conduct reconciliation in their records?

A bank reconciliation is used to compare your records to those of your bank, to see if there are any differences between these two sets of records for your cash transactions. Thus, fraud detection is a key reason for completing a bank reconciliation. …

How is an NSF check treated in a bank reconciliation?

NSF (not sufficient funds) checks. When this happens, the bank returns the check to the depositor and deducts the check amount from the depositor’s account Therefore, NSF checks must be subtracted from the company’s book balance on the bank reconciliation.

Which account is the main focus of a bank reconciliation?

Balance sheet accounts are usually the focus of reconciliations. These accounts include information about the company’s assets and liabilities. Business managers use reconciliations as part of their cash management process. Bank reconciliations review company’s internal cash information against the bank statement.

How expenses are recognized?

The accounting method the business uses determines when an expense is recognized. If the business uses cash basis accounting, an expense is recognized when the business pays for a good or service. Under the accrual system, an expense is recognized once it is incurred.

What are the five steps to reconciling a bank statement?

Once you’ve received it, follow these steps to reconcile a bank statement:

- COMPARE THE DEPOSITS. Match the deposits in the business records with those in the bank statement.

- ADJUST THE BANK STATEMENTS. Adjust the balance on the bank statements to the corrected balance.

- ADJUST THE CASH ACCOUNT.

- COMPARE THE BALANCES.

What is the first step in the reconciliation process?

Here are the steps for completing a bank reconciliation:

- Get bank records.

- Gather your business records.

- Find a place to start.

- Go over your bank deposits and withdrawals.

- Check the income and expenses in your books.

- Adjust the bank statements.

- Adjust the cash balance.

- Compare the end balances.

Why does a business prepare a bank reconciliation?

Bank reconciliation statements ensure payments have been processed and cash collections have been deposited into the bank. The reconciliation statement helps identify differences between the bank balance and book balance, in order to process necessary adjustments or corrections.