Which accounting standard is for depreciation?

IAS 16 defines depreciation as ‘the systematic allocation of the depreciable amount of an asset over its useful life’. The ‘depreciable amount’ is the cost of an asset, cost less residual value, or other amount (for example the revaluation of the asset).

Which accounting standards is applicable for fixed assets?

17.1 Certain specific disclosures on accounting for fixed assets are already required by Accounting Standard 1 on ‘Disclosure of Accounting Policies’ and Accounting Standard 6 on ‘Depreciation Accounting’.

Which as is applicable for depreciation?

Depreciation under AS 10 Property, Plant and Equipment Depreciable amount of any asset should be allocated on a methodical basis over the useful life of the asset. Every part of property or P&E (Plant and Equipment) whose cost is substantial with respect to the overall cost of the item must be depreciated separately.

What legislation and accounting standard applies to depreciation?

According to paragraph 50 of AASB 116, the depreciable amount of an asset is the amount which must be allocated on a systematic basis over the asset’s estimated useful life. The amount of depreciation expense is to be recognised in the profit and loss statement.

How do you depreciate a revalued asset?

In simple terms the revalued amount should be depreciated over the assets remaining useful life. The depreciation charge on the revalued asset will be different to the depreciation that would have been charged based on the historical cost of the asset.

Can fixed assets be expensed?

Fixed assets are capitalized. That’s because the benefit of the asset extends beyond the year of purchase, unlike other costs, which are period costs benefitting only the period incurred. Fixed assets should be recorded at cost of acquisition. Fixed assets that cost less than the threshold amount should be expensed.

Is depreciation mandatory under Companies Act?

Companies are required to calculate depreciation as per Companies Act as well as Income Tax Act. Such extra depreciation cannot be claimed under the provisions of income tax except additional depreciation in the year of purchase on new plant and machinery used for manufacture.

What is the standard depreciation?

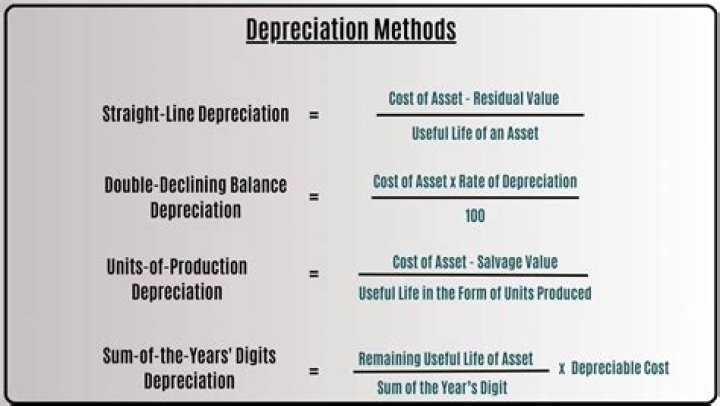

Straight line depreciation is a common method of depreciation where the value of a fixed asset is reduced gradually over its useful life. The default method used to gradually reduce the carrying amount of a fixed asset over its useful life is called Straight Line Depreciation.

What is the formula of excess depreciation?

The ‘excess depreciation’ is the difference between the new depreciation (based on the revalued amount) and the previous depreciation (based on the original cost).

What is depreciation rate as per Companies Act?

I. Buildings

| Nature of assets | Useful life as per companies act | Depreciation rate |

|---|---|---|

| Buildings (other than factory buildings) other than RCC Frame Structure | 30 years | 9.50 % |

| Factory buildings | 30 years | 9.50 % |

| Fences, wells, tube wells | 5 years | 45.07 % |

| Others (including temporary structure, etc.) | 3 years | 63.16 % |