Which book is both journal and ledger?

cash book

A cash book serves the purpose of both the journal and ledger, whereas a cash account is structured like a ledger.

Is cash book a journal or a ledger explain?

Cash Book is both a Journal and a ledger: It is a subsidiary book because all cash transactions are, first recorded in the cash book and then from cash book posted to various accounts in the ledger. The recording of transactions in the cash book takes the shape of ledger account.

Why cash book is journal?

In a cash book like journal, the transactions are recorded in chronological order. This is due to the fact that basic transactions can be transferred to the Ledger. The cash book, like the journal, includes an explanation of the transaction. Transactions from the cash book are also recorded in a ledger.

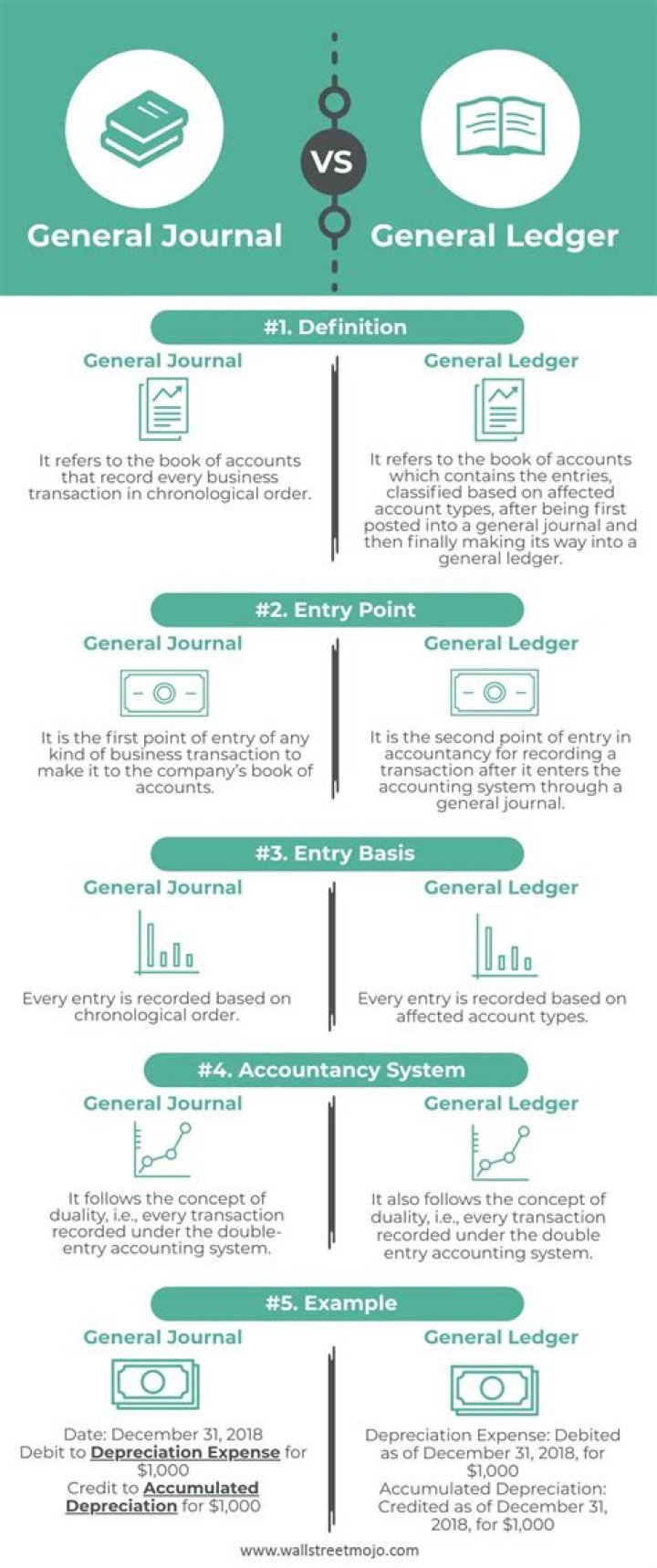

Is ledger and journal the same?

The journal is the first step of the accounting cycle because all transactions are analyzed and recorded as journal entries. The ledger is an extension of the journal where journal entries are marked by the company and its general ledger account based on which of the financial statements the company has prepared.

Why is cash book kept separate and not in the general ledger?

Among the financial transactions of concern, cash transactions carry much more importance. That’s why these are recorded in a separate book of account. Since all cash transactions are recorded in this book in the ledger account format, a separate cash account in the ledger is not needed.

How do I keep my cashbook manually?

Maintenance of Cash Book

- All monetary transactions should be entered in the cash book as soon as they occur (SR 31).

- Cheque/ Draft should be considered as cash.

- Cash book should be closed and balanced each day.

- DDO should verify all entries in the cash book with original documents viz.

What is journal proper example?

Definition and Explanation: Journal proper is book of original entry (simple journal) in which miscellaneous credit transactions which do not fit in any other books are recorded. It is also called miscellaneous journal. The form and procedure for maintaining this journal is the same that of simple journal.

What is the purpose of journal proper?

A Journal proper is used for recording those transactions which do not find a place in any other subsidiary book such as Cash Book, Purchases Book, Sales Book, Bills Payable Book, etc.