Which method does not deduct residual value in calculating depreciation?

The double-declining balance method. When a company uses this method, they take the asset’s cost minus the accumulated depreciation and use that number as the value. They do not deduct the residual value which is the left over value after it has been fully depreciated.

Which depreciation method does not use salvage value?

declining-balance depreciation method

The declining-balance depreciation method Don’t deduct salvage value when figuring the depreciable base for the declining balance method.

Which of the following is not the method of depreciation of assets?

Land, although a fixed asset is never depreciable. It has an unlimited useful life and therefore can not be depreciated. Depreciation is allocation of cost of fixed asset over its useful life. Value of land can not be reduced to zero and it can not be allocated over its useful life.

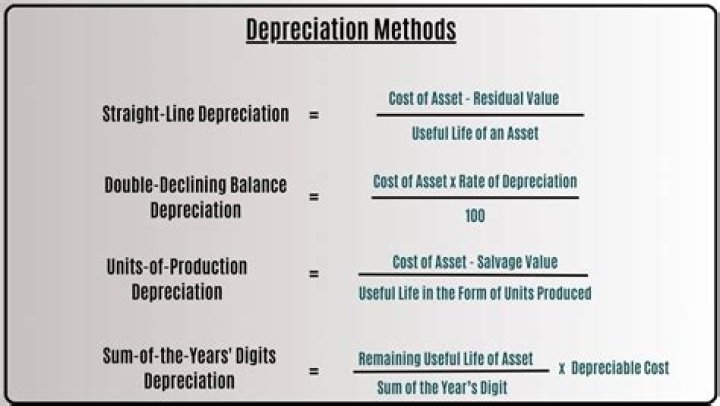

What is the double declining depreciation method?

The double declining balance depreciation method is an accelerated depreciation method that counts as an expense more rapidly (when compared to straight-line depreciation that uses the same amount of depreciation each year over an asset’s useful life).

What if residual value is not given?

The most common option for lower-value assets is to conduct no residual value calculation at all; instead, assets are assumed to have no residual value at their end-of-use dates. However, the resulting amount of depreciation recognized will be higher than would have been the case if a residual value had been used.

Does reducing balance method use residual value?

To calculate reducing balance depreciation, you will need to know: Asset cost: the original value of the asset plus any additional costs required to get the asset ready for its intended use. Residual value: also known as scrap or salvage value, this is the value of the asset once it reaches the end of its useful life.

How do you calculate a double declining rate?

First, Divide “100%” by the number of years in the asset’s useful life, this is your straight-line depreciation rate. Then, multiply that number by 2 and that is your Double-Declining Depreciation Rate. In this method, depreciation continues until the asset value declines to its salvage value.

How do I calculate residual value?

In the case of leasing, the lessor determines the residual value based on future estimates and past models. Calculating residual value requires two figures namely, estimated salvage value and cost of asset disposal. Residual value equals the estimated salvage value minus the cost of disposing of the asset.

How do you calculate reducing balance depreciation and residual value?

Depreciation per annum = (net book value – residual value) x depreciation factor (rate %). Subtract the depreciation charge from the current book value to calculate the remaining book value.

Which is the simplest equation for residual valuation?

The numbers that go behind the equation may be seem complicated at first, but once these factors have been determined, the residual valuation method is a fairly straightforward calculation to perform, and yet highly useful. Without further ado, the equation for the residual valuation method in its simplest form is as follows:

How is residual valuation used to value land?

As such, this article aims to provide you with a basic overview and simple method to derive the value of the land. The residual valuation method – this is the approach taken to conveniently assess the value of a development site or land that has the potential to be developed or redeveloped.

Can a residual income method be used to value a company?

The residual income valuation approach is a viable and increasingly popular method of valuation and can be implemented rather easily by even novice investors. When used alongside the other popular valuation approaches, residual income valuation can give you a clearer estimate of what the true intrinsic value of a firm may be.

Which is a component of the residual method?

A further explanation for the aforesaid components to the residual method of valuation calculation are described in detail below: Gross Development Value (commonly known as GDV as well) is an integral part of the residual method of valuation equation and is something that property developers always attempt to determine right from the get-go.