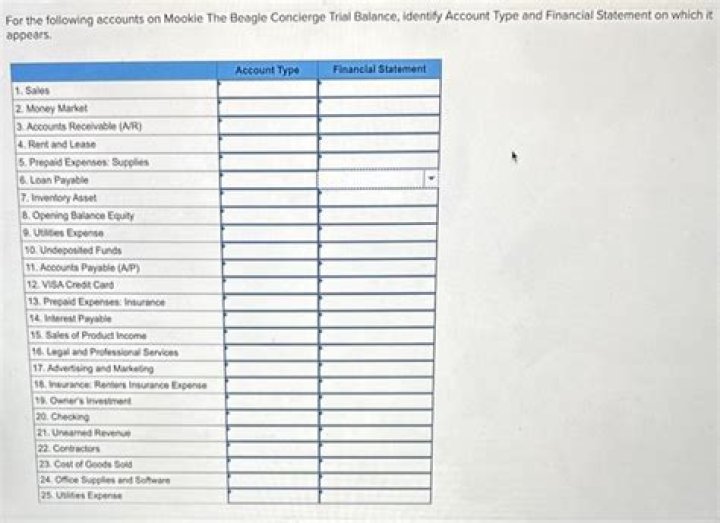

Which of the following accounts are closed at the end of the accounting period?

Nominal accounts are accounts that are closed at the end of the accounting period. These accounts are typically the income and expense accounts that are presented in the income statement.

What accounts are closed at the end of the accounting period quizlet?

Temporary accounts refer to accounts that are closed at the end of every accounting period. These accounts include revenue, expense, and withdrawal accounts. They are closed to prevent their balances from being mixed with those of the next period. Also known as: Nominal accounts, Income statement accounts.

Are all balance sheet accounts permanent?

Also referred to as real accounts. Accounts that do not close at the end of the accounting year. The permanent accounts are all of the balance sheet accounts (asset accounts, liability accounts, owner’s equity accounts) except for the owner’s drawing account.

Do balance sheets have zero balances after the closing entries have been posted?

Posting closing entries: Once all closing entries are complete, the information is transferred to the general ledger T-accounts. Balances in temporary accounts will show a zero balance.

How do you record closing journal entries?

Four Steps in Preparing Closing Entries

- Close all income accounts to Income Summary.

- Close all expense accounts to Income Summary.

- Close Income Summary to the appropriate capital account. Owner’s capital account for sole proprietorship.

- Close withdrawals/distributions to the appropriate capital account.

Which account is closed at the end of the accounting period with a debit?

income summary account

Close the income statement accounts with debit balances (normally expense accounts) to the income summary account. After all revenue and expense accounts are closed, the income summary account’s balance equals the company’s net income or loss for the period.

Which accounts are closed at the end of the accounting period Why is it necessary to close these accounts?

Closing entries: Closing entries prepare a company for the next period and zero out balance in temporary accounts. Purpose of closing entries: Closing entries are necessary because they help a company review income accumulation during a period, and verify data figures found on the adjusted trial balance.

What kind of accounts are closed at the end of the year?

Conversely, permanent accounts accumulate balances on an ongoing basis through many fiscal years, and so are not closed at the end of the fiscal year. The most common types of temporary accounts are for revenue, expenses, gains, and losses – essentially any account that appears in the income statement.

When do temporary accounts get closed in accounting?

PRO Features Log In. The temporary accounts get closed at the end of an accounting year. Temporary accounts include all of the income statement accounts (revenues, expenses, gains, losses), the sole proprietor’s drawing account, the income summary account, and any other account that is used for keeping a tally of the current year amounts.

How are nominal accounts closed at period end?

Nominal or temporary accounts are closed in the following way: The credit accounts (i.e. revenue accounts) are closed by making a debit entry to the account and a credit entry to Income Summary. The debit accounts (i.e. expense accounts) are closed by making a credit entry to the account and a debit entry to Income Summary.

What happens at the end of an accounting period?

To prepare the financial statements at the end of an accounting period, a number of actions should be taken which represent closing the books. Closing the books process can be illustrated in the following way: The illustration above is one of the variations of the closing process.