Which requirement must be satisfied in order to specially allocate partnership income or losses to partners?

Which requirement must be satisfied in order to specially allocate partnership income or losses to partners? Special allocations must reduce the combined tax liability of all the partners. Special allocations must be insignificant. At least one partner must agree to the special allocations.

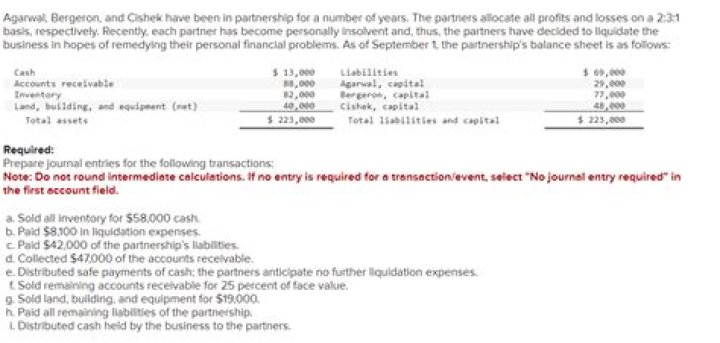

How are partnership profits and losses allocated?

In a partnership, profits and losses typically get distributed to owners of the business based on their percentage interests in the partnership. For example, imagine a business that has a partnership structure with four partners: Partner A, Partner B, Partner C, and Partner D.

Can depreciation be specially allocated?

While the preceding description of a special allocation arrangement is often accurate, you can also have special allocations of specific tax items, such as depreciation, rather than special allocations of overall partnership losses.

Is it possible to allocate profit or loss to partners based solely on salaries?

It is possible to allocate profit and loss to partners based solely om salaries. In certain cases when distribution of profits or losses involves salary and interest allowances, some partners may receive an increase in equity and others may suffer a decrease.

How is depreciation allocated in a partnership?

Regulations require that all partners (other than the contributing partner) be allocated depreciation based upon the fair market value of the property at the time of the contribution. Thus, the partnership steps into the shoes of the transferor and can only depreciate the asset over its remaining useful life.

How are special allocations used in a partnership agreement?

Rather than assigning the partner a larger percentage of ownership in the partnership agreement, the company can make use of special allocations to pay that partner a larger percentage of the profits in order to repay the higher level of initial investment.

When do you need a special allocation in a LLC?

However, there are some situations in which there may be a need for a special allocation. For example, if Partner A provided all of the startup income for the business, the partnership agreement (or an operating agreement in an LLC) might stipulate that Partner A will be allocated 75 percent of the business profits and losses the first year.

Is the special allocation of net business income proper?

This special allocation did not conform with the partnership agreement; therefore, the “partnership agreement does not support [the taxpayer’s] claim that the special allocation of the net business income of the [partnership] . . . is proper.”

Can a partnership be taxed according to percentages?

If the IRS does not believe that the special allocation is legitimate, it can tax all of the partners according to their percentage interests in the business even if there is another agreement—such as your partnership agreement—that says otherwise.