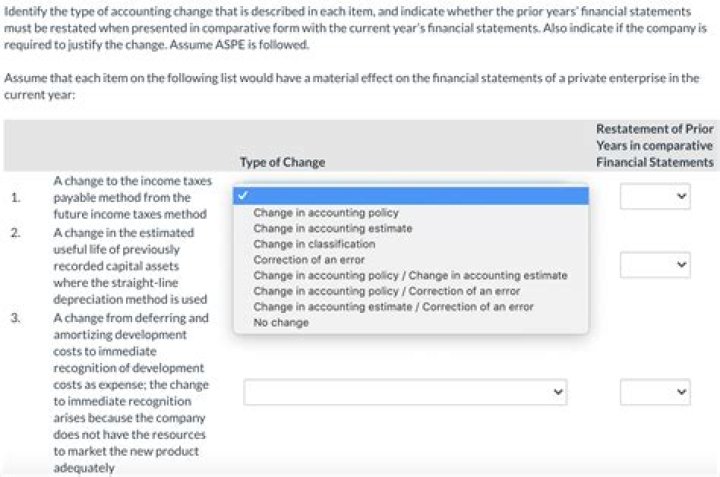

Which type of accounting change is accounted for in current and future periods?

– Retrospective — When we are required to change prior year statements. – Prospective — Adjusting the current and future estimates. Each change/correction is accounted for under specified method as prescribed by the accountancy regulatory body.

Which type of accounting change should always be?

Changes in accounting principle are always handled in the current or prospective period. b. Prior statements should be restated for changes in accounting estimates.

Which of the following disclosures is required for a change from sum of the years digits to straight-line depreciation method?

credit to Accumulated Depreciation. Which of the following disclosures is required for a change from sum-of-the-years-digits to straight-line? debit to Retained Earnings in the amount of the difference on prior years, net of tax.

What are the proper time periods to record the effects of a change in accounting estimate?

Hence, the proper time period, to record the effect of a change in accounting estimates is Current Period and Prospectively.

Which is a change in accounting policy?

Changes in accounting policies is required by a standard or interpretation; or. results in the financial statements providing reliable and more relevant information about the effects of transactions, other events or conditions on the entity’s financial position, financial performance, or cash flows. [IAS 8.14]

Which of the following is treated as a change in accounting principle?

Adopt a new FASB standard. An example of a change in accounting estimate that is effected by a change in accounting principle is a change in: depreciation methods.

How should the effect of a change in accounting estimate be accounted for?

How should the effect of a change in accounting estimate be accounted for? a. By restating amounts reported in financial statements of prior periods.

Which of the following is an example of a change in accounting policy?

ABC LTD until now has valued inventory using LIFO method. However, following changes to IAS 2 Inventories, the use of LIFO method has been disallowed. Therefore, management of the company intends to use FIFO method for the valuation of the company’s stock.

Which of the following is a good example of changes in accounting principles?

Following are a few examples of changes in accounting principles: Any change in method used to account for inventory valuation i.e. the cost flow assumption, for e.g. any change from FIFO to weighted average method and vice versa.

Which of the following should be considered a direct effect of a change in accounting policy?

(a) Deferred taxes is a direct effect from the change in accounting principle, and its effects should be recorded in the earliest period presented, if practicable. Profit sharing and royalty payments are indirect effects and should be reported in the period of the change.