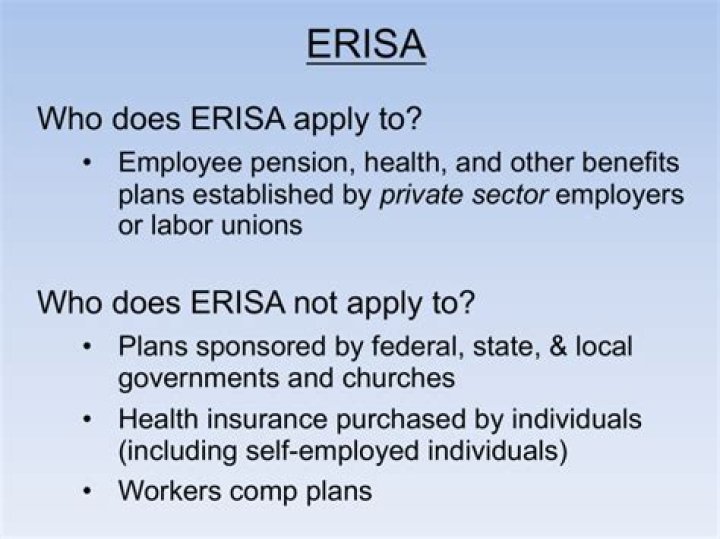

Who does ERISA not apply to?

In general, ERISA does not cover group health plans established or maintained by governmental entities, churches for their employees, or plans which are maintained solely to comply with applicable workers compensation, unemployment, or disability laws.

Who is subject to Title 1 of ERISA?

The provisions of Title I of ERISA cover most private sector employee benefit plans. Such plans are voluntarily established or maintained by an employer, an employee organization, or jointly by one or more such employers and an employee organization.

What plans does ERISA apply to?

ERISA applies to two types of plans – “Employee Welfare Benefit Plans” and “Employee Pension Benefit Plans.”

What are the ERISA rules?

ERISA requires plans to provide participants with plan information including important information about plan features and funding; sets minimum standards for participation, vesting, benefit accrual and funding; provides fiduciary responsibilities for those who manage and control plan assets; requires plans to …

What is an ERISA violation?

A violation occurs when a company fails to meet its ERISA obligations. While there are many types of violations, some of the most common include: — Interference with employee rights. — Improperly denying benefits to a former or current employee. — Breach of fiduciary duty.

What retirement plans are not covered by ERISA?

Government employee plans and IRAs do not. ERISA was enacted in the 1970s to protect the retirement income of workers in the private sector.

What employers are subject to ERISA?

ERISA applies to private-sector companies that offer pension plans to employees. This includes businesses that: Are structured as partnerships, proprietorships, LLCs, S-corporations and C-corporations. No matter how your employer has structured his or her business, it is covered by ERISA if it is a private entity.

Who enforces ERISA?

ERISA is administered and enforced by three bodies: the Labor Department’s Employee Benefits Security Administration, the Treasury Department’s Internal Revenue Service, and the Pension Benefit Guaranty Corporation.

How does ERISA affect insurance?

ERISA restricts the ability of states to enact laws that relate to employee welfare benefits, including employer-sponsored health insurance coverage. Under “self- funded” or “self-insured” plans, the employer is actually responsible for paying most of the health bills—not just the insurance premiums.

Who is required to follow ERISA regulations?

Most employer-sponsored plans, such as a 401(k), fall under ERISA. Government employee plans and IRAs do not. ERISA was enacted in the 1970s to protect the retirement income of workers in the private sector.

What do you need to know about the ERISA law?

The ERISA Law is the Employee Retirement Income Security Act of 1974. This federal law applies to almost all private employers except for those who qualify for exemption. Put simply, this law describes standards for pension plans, welfare benefits like health and life insurance, apprenticeship plans, and disability insurance.

How does ERISA apply to privately purchased insurance?

Privately purchased insurance plans don’t apply, as ERISA only affects plans offered by employers. The Benefit Claims Procedure Regulation additionally regulates ERISA and determines what benefits can be granted to employees who file claims or appeals. What Are Provisions Under ERISA?

Who is liable for an ERISA plan failure?

Insurance documents for ERISA plans indicate the employer as the sponsor, agent for service, administrator, and fiduciary for the plan. Under ERISA, the employer is liable for all plan failures including failure to comply.

Who is a participant in the ERISA program?

A participant is a current or former employee who has qualified for ERISA benefits or could become qualified in the near future. This also works if their beneficiaries are eligible. Beneficiaries who qualify for COBRA and covered retirees can still be considered participants. Participants are not necessarily beneficiaries.