Who is the beneficiary on a key person insurance policy?

Under a key person life insurance policy, the business owns the policy, pays the premiums and is the beneficiary. If a key person dies, the business then collects a death benefit.

Who is typically the beneficiary of a key employee life insurance plan?

Typically, the business owns the policy, pays the premiums, and is the beneficiary of the key employee life insurance policy. Since the business owns the life insurance covering the key person, it has control of the policy. Policy cash values and death benefits may be used by the business for any purpose.

Who owns a key man policy?

Typically, the company pays premiums for the key person policy, and also owns it and is the beneficiary, says the III. The key employee must provide consent, in writing, to your company owning the policy.

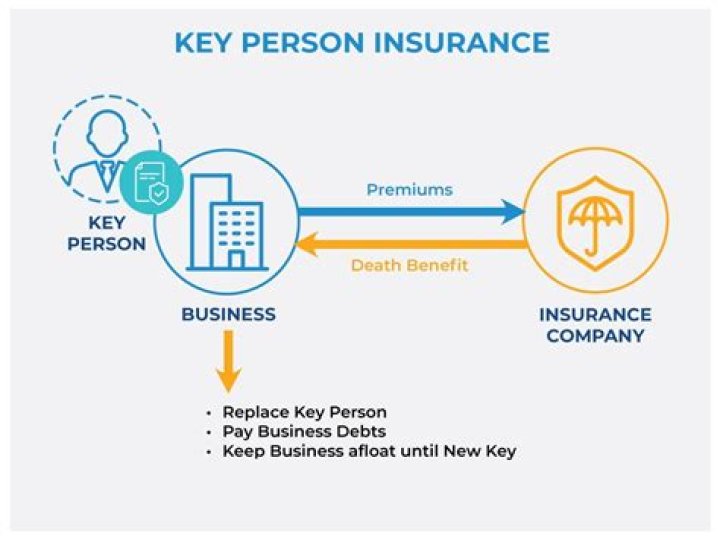

Who is the owner and who is the beneficiary on a key person life insurance?

In Key Person Insurance, the company is the owner, the key person is the insured, and the beneficiary is also the company.

Are key man life insurance premiums deductible?

Typically, the cost of key man life insurance is not tax deductible. Premiums must be paid with after-tax dollars. Your company can only deduct key man insurance premiums if they’re considered to be part of the employee’s taxable income, in which case the employee is typically the beneficiary.

What is the purpose of key person life insurance?

Key person life insurance provides a relatively inexpensive means of covering costs of replacing a deceased executive, but it also provides re-assurance to the company’s creditors by ensuring that the death does not threaten the company’s survival.

How much does a key man policy cost?

Costs for a key man policy may range from $100 to $2,000 per month. Most small businesses can’t afford to go without key person insurance and, in many cases, partners or lenders require you to have a policy to protect everyone’s interest in the company.

What is a key man risk?

Much has been written about ‘key man’ risk — the danger for corporations that rely on one or a few individuals — and its impact on business value. Fashion firms with a celebrity designer, for example, or asset management firms with a star investment manager, are particularly vulnerable.

Which is the best reason to purchase life insurance rather than annuities?

The annuity offers tax-deferred savings and retirement income. Simply put—life insurance protects your loved ones if you die prematurely while the annuity protects your income if you live longer than expected.

Is death a benefit?

A death benefit is a payout to the beneficiary of a life insurance policy, annuity, or pension when the insured or annuitant dies. For life insurance policies, death benefits are not subject to income tax and named beneficiaries ordinarily receive the death benefit as a lump-sum payment.

Who is the beneficiary of key man insurance?

The company is the beneficiary of the policy and pays the premiums. This type of life insurance is also known as “key man (or “keyman”) insurance,” “key woman insurance,” and “business life insurance.”

How is key man life insurance different from other life insurance?

Key man life insurance differs from other life insurance policies in that the business is both the owner and the beneficiary of the policy. The employee essentially has no rights or active participation in the policy.

Can a key man policy be used as an employee benefit?

A key man policy can also be used as an employee benefit, since the life insurance policy can be transferred to the executive or insured employee by the company. Though key person life insurance premiums aren’t tax deductible, the proceeds of the policy are usually provided to the company free of income tax.

How does tax treatment work for key man life insurance?

Tax Treatment for Employees. If your company is the sole owner and beneficiary of a key person life insurance policy, there are no tax implications for the insured employee. Policy premiums aren’t considered as part of the insured’s taxable income unless they have ownership in the policy or would be a beneficiary.