WHO issues debit and credit note?

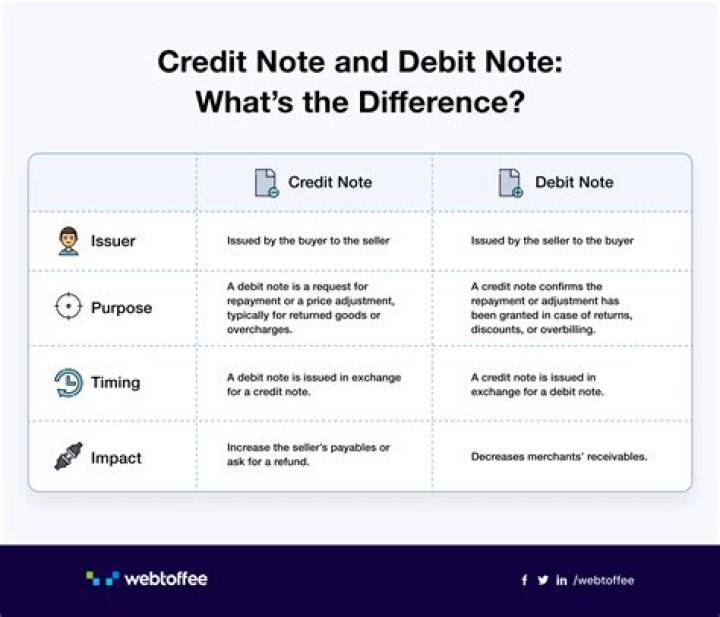

A debit note is issued by the customer or buyer of the goods to the supplier or the seller of the goods whereas a credit note is issued by the supplier or the seller of the goods to the customer or buyer of the goods.

Can seller issue debit note?

A debit note (also known as debit memo) can be issued from a buyer to their seller to indicate or request a return of funds due to incorrect or damaged goods received, purchase cancellation, or other specified circumstances.

Can purchaser issue debit note under GST?

Credit notes and debit notes cannot be issued by recipients with GST. It is a unidirectional flow from supplier. Multiple credit or debit notes for one tax invoice is permissible. One credit note or debit note for multiple tax invoices are also allowed.

Can we issue credit note against debit note?

A downward revision can be done using a credit note, while one can make an upward revision with a supplementary invoice or debit note. However, when a registered person has to issue an invoice for the supplies made before obtaining registration, it is called a ‘revised invoice’.

Can we claim ITC on debit note?

The said amendment has been introduced to delink the invoice and debit note for the purpose of claiming ITC. In light of the above provisions, it can be concluded that ITC shall be available on the debit notes which are issued in the following financial years of the corresponding invoice.

Is debit note taxable?

Output Tax Liability of Supplier A debit note issued by the supplier increases the output tax liability of the supplier. This is on account of the value of taxable goods charged in the invoice to be less than the actual delivery of goods or services.

What is debit note entry?

Debit Note is a document/voucher given by a party to other party stating that such other party’s account is debited in the books of sender. For example: A trader “ABC” purchases goods from “XYZ”. Therefore ABC sends a debit note amounting to Rs. 10,000 to XYZ stating that he has debited his account in his books.

What is the time limit for taking ITC?

To claim ITC, the buyer should pay the supplier for the supplies received (inclusive of tax) within 180 days from the date of issuing the invoice.

How much ITC can be claimed?

As per the sub-rule (4) inserted in rule 36 of the Central Goods and Service Tax Rules, 2017, a taxpayer filing GSTR-3B can claim provisional Input Tax Credit (ITC) only to the extent of 5% of the eligible credit available in GSTR-2B (earlier, GSTR-2A was considered).

What is TCS debit note?

TCS to be collected when you receive payment more than Rs. 50 lacs that means when you receive the payment. So, TCS NOT TO BE INCLUDED in INVOICE. The TCS can be collected by charging through debit note in the month end, when you receive payment.

Can we show debit note in gstr1?

The reporting of credit/debit notes on the GST portal was made in GSTR-1. It can be classified as follows: Credit note/debit note issued to unregistered persons (B2C supplies): It must be declared in Table ‘9B – Credit/Debit Notes (Unregistered)’.

What are the eligibility criteria for input tax credit?

Sec 16(1) Eligibility Criteria:- Persons should be registered person to take ITC. Goods or Services are used/intended to be used in the course or furtherance of business. The amount should have Credited to Electronic Ledger of such person.

Can we take ITC on television?

GST ITC not claimed on Television Here the T.V is being used for business purpose and not for personal use and is therefore allowed to be claimed as ITC on purchase from a registered GST dealer on receiving an appropriate GST invoice for the same.

What are ineligible ITC?

ITC used for business purposes will be declared as eligible ITC and those used for other purposes will not be able to claim as ITC except blocked credit, which are specifically provided separately. The ITC eligibility is based on whether the same is used for taxable supplies or exempt supplies.

What qualifies as an ITC?

You may be eligible to claim ITCs only to the extent that your purchases and expenses are for consumption, use, or supply in your commercial activities. To claim an ITC, the expenses or purchases must be reasonable in quality, nature, and cost in relation to the nature of your business.