Why do we focus on cash flow as opposed to net income in capital budgeting?

We focus on cash flows rather than accounting profits because these are the flows that the firm receives and can reinvest. Only by examining cash flows are we able to correctly analyze the timing of the benefit or cost. Thus, accounting profits become lower and, in turn, so do taxes, which are a cash flow item.

Is cash flow more important than net income?

Although many investors gravitate toward net income, operating cash flow is often seen as a better metric of a company’s financial health for two main reasons. First, cash flow is harder to manipulate under GAAP than net income (although it can be done to a certain degree).

Why is cash flow used in capital budgeting?

The identification of cash inflows and outflows is a means of making the impact of a capital investment project readily apparent to interested parties. Cash budgeting is also used to determine if project goals are realistic and realizable in light of allotted resources.

What’s the difference between net income and operating cash flow?

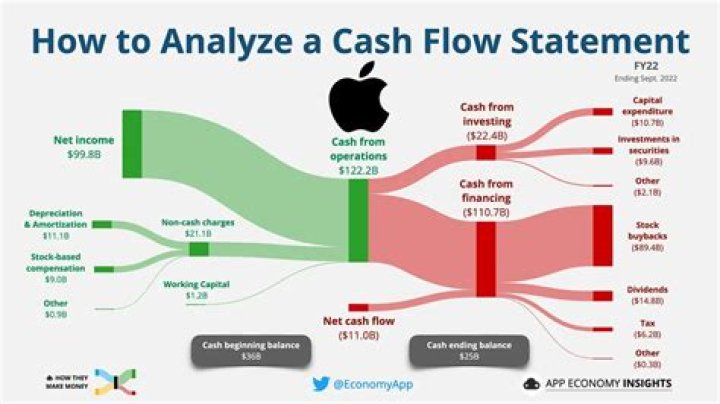

Operating flows – The net cash generated from operations (net income and changes in working capital). Investing flows – The net result of capital expenditures, investments, acquisitions, etc. Financing flows – The net result of raising cash to fund the other flows or repaying debt.

Why do we focus on cash flows instead of profits?

First things first, these are not just cash flows but incremental cash flows after tax i.e. additional cash flows after tax which emanate from the new project undertaken.

Which is the net result of investing and financing flows?

Investing flows – The net result of capital expenditures, investments, acquisitions, etc. Financing flows – The net result of raising cash to fund the other flows or repaying debt.

Which is the best method for discounting cash flows?

The two most common techniques involved in discounting cash flows are net present value and internal rate of return. While the discounted cash flow models are the ideal, I would also want to forecast or project the impact on the company’s future financial statements.