Why does liability account increase with credit?

A credit increases the balance of a liabilities account, and a debit decreases it. In this way, the loan transaction would credit the long-term debt account, increasing it by the exact same amount as the debit increased the cash on hand account.

Does liability increase debit or credit?

Liability accounts normally have credit balances. Thus, if you want to increase Accounts Payable, you credit it. If you want to decrease Accounts Payable, you debit it. The same rules apply to all asset, liability, and capital accounts.

What account types increase with a credit?

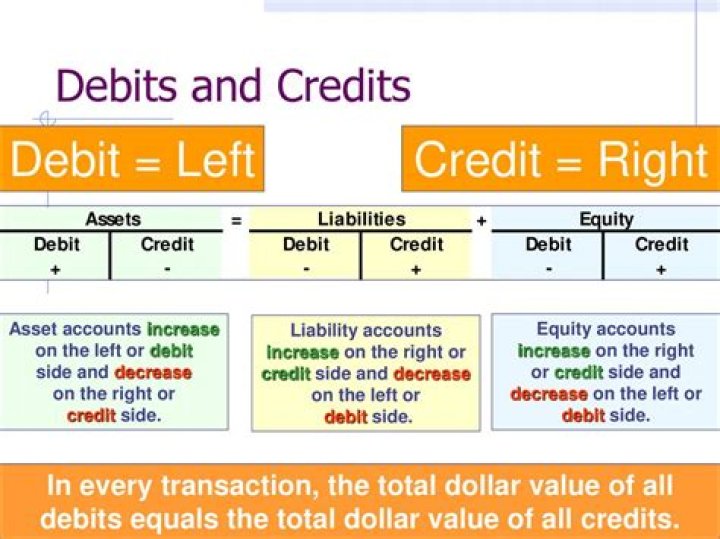

Debits and credits chart

| Debit | Credit |

|---|---|

| Increases an asset account | Decreases an asset account |

| Increases an expense account | Decreases an expense account |

| Decreases a liability account | Increases a liability account |

| Decreases an equity account | Increases an equity account |

Can you debit an asset and credit a liability?

Debits increase asset and expense accounts. Debits decrease liability, equity, and revenue accounts.

What are the factors that will increase an owner’s equity?

The main accounts that influence owner’s equity include revenues, gains, expenses, and losses. Owner’s equity will increase if you have revenues and gains. Owner’s equity decreases if you have expenses and losses. If your liabilities become greater than your assets, you will have a negative owner’s equity.

Do liabilities increase with a debit or credit?

Liability Accounts Increases are debits and decreases are credits. You would debit notes payable because the company made a payment on the loan, so the account decreases.

Why do asset accounts increase with a debit?

Assets and expenses have natural debit balances. This means positive values for assets and expenses are debited and negative balances are credited. In effect, a debit increases an expense account in the income statement, and a credit decreases it. Liabilities, revenues, and equity accounts have natural credit balances.

Why liabilities are credited?

Definition of liability accounts Liability accounts are categories within the business’s books that show how much it owes. A debit to a liability account means the business doesn’t owe so much (i.e. reduces the liability), and a credit to a liability account means the business owes more (i.e. increases the liability).

What happens when you credit a liability account?

A debit to a liability account means the business doesn’t owe so much (i.e. reduces the liability), and a credit to a liability account means the business owes more (i.e. increases the liability).

What increases with a debit?

A debit is an entry made on the left side of an account. It either increases an asset or expense account or decreases equity, liability, or revenue accounts. It either increases equity, liability, or revenue accounts or decreases an asset or expense account.

How is an increase in an asset credited or debited?

Increase in the asset is debited and the decrease in the asset is credited while the increase in liability is credited and the decrease in liability is debited. Whether a debit increase or decreases, an account depends on what kind of account it is. In the accounting equation: Assets = Liabilities + Equity

Can a debit or credit increase the balance on an expense account?

There are some exceptions, such as increasing one asset account while decreasing another asset account. If you are more concerned with accounts that appear on the income statement, then these additional rules apply: Revenue accounts. A debit decreases the balance and a credit increases the balance. Expense accounts.

How does debit and credit work in accounting?

Asset = Equity + Liability. Increase in the asset is debited and the decrease in the asset is credited while the increase in liability is credited and the decrease in liability is debited. Whether a debit increase or decreases, an account depends on what kind of account it is. In the accounting equation: Assets = Liabilities + Equity

Do you use increase or decrease in accounting?

However, we do not use the concept of increase or decrease in accounting. We use the words “debit” and “credit” instead of increase or decrease. The meaning of debit and credit will change depending on the account type.