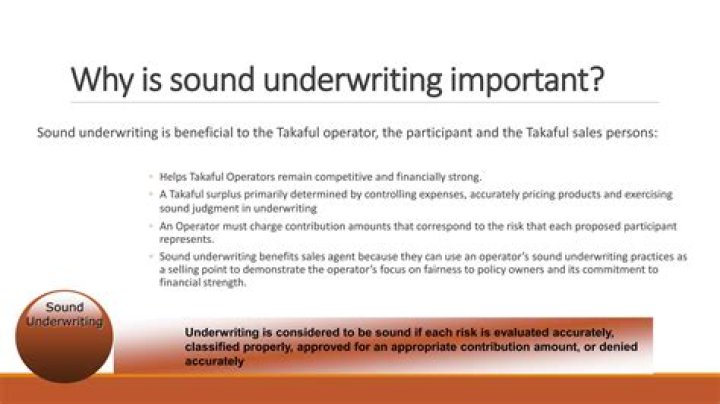

Why is sound underwriting important?

Sound underwriting standards protect financial institutions from excessive risks that can lead to losses. History indicates that lending and underwriting standards are generally pro-cyclical. During that same crisis, many companies also tightened underwriting standards (one of the culprits in the downturn).

Why do you think underwriting is necessary for an insurance company?

Description: Underwriting is a critical risk mitigation mechanism adopted in the insurance industry. The process helps in deciding the appropriate premium for an insured. The underwriter needs to match the premium received with the claims paid with an eye on profitability.

What is the main purpose of insurance underwriters?

Insurance underwriters are professionals who evaluate and analyze the risks involved in insuring people and assets. Insurance underwriters establish pricing for accepted insurable risks. The term underwriting means receiving remuneration for the willingness to pay a potential risk.

What is underwriting risk and how does it relate to insurance companies?

Underwriting risk is the risk of uncontrollable factors or an inaccurate assessment of risks when writing an insurance policy. If the insurer underestimates the risks associated with extending coverage, it could pay out more than it receives in premiums.

Are underwriters strict?

Back between 2002 and 2008, guidelines for underwriters were fairly loose. Today, trained underwriters follow strict black-and-white guidelines intended to protect borrowers from taking on more mortgage responsibility than is safe for them.

What is risk based underwriting?

Lenders and other financial institutions such as insurance companies use “risk-based” underwriting to either set or adjust the price and other credit conditions for a particular borrower or client based on that person’s credit history.

What makes a great insurance underwriter?

Van Leunen believes that what makes a good underwriter is asking questions to, in her words, “soak up the knowledge” of experienced coworkers. “When I have downtime in the office, I will go to more senior people and pick their brains, listen to their stories and learn from them,” she says.

What do insurance companies need to know about underwriting?

An insurance company must have a way to decide just how much of a gamble it’s taking by providing coverage. It also needs to know the chances that something will go wrong, causing it to have to pay out a claim. For instance, a payout may be nearly assured if a company is being asked to insure a person who has cancer.

What to do if you are unhappy with an underwriting decision?

If you’re unhappy with an underwriting decision and your insurance agentor broker can’t resolve the problem for you, you can contact your state insurance commissioner’s office, or ask your agent if the insurance company has an ombudsman who you may be able to speak to get involved on your behalf.

What happens if an underwriter is not comfortable with a risk?

If an underwriter is not comfortable with a risk, they may deny or cancel the insurance policy. It’s not an underwriter’s job to speak to the insured, but only to the agents or brokers who are responsible for passing the information onto their clients.

Why do insurance companies deny and devalue claims?

The insurance adjuster for the other side, however, is not there to help you. They solely exist to protect and promote the interests of their employer – the insurance company. The insurance company’s ultimate goal is to pay out nothing or as little as possible on every claim – that is, to deny and devalue claims.